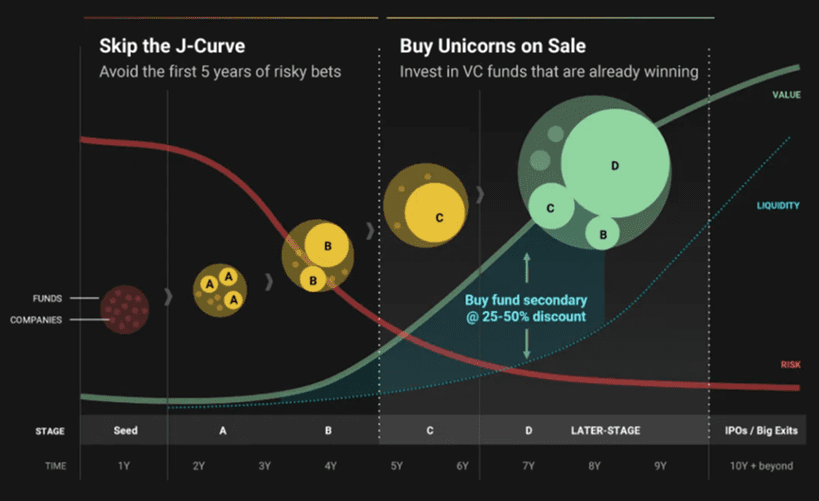

PVC, a sort of funds of funds when it comes to venture capital funds, has beautifully captured a value creation opportunity in venture capital fund investments.

“Because portfolio companies are already established and growing, buyers have a better sense of what they’re getting for their money – they aren’t investing in a “blind pool” of unknown future assets. After five years or more, successful VC funds should have established winners at Series B or C and perhaps even early exits and distributions. Seeing the first few years of performance in the rearview mirror provides insight into how well the fund manager is doing and how well the fund is likely to perform in the future. Again, it’s kind of like checking the score at halftime to see which team is ahead.”

But their model assumes a particular growth pattern underlying the growth of the portfolio startups. Something distinctly not present in the heavily regulated world of healthcare startups. Value creation for healthcare focused funds, therefore, should focus more on the relationship between the regulators and innovators, and draw growth patterns focused more on the dynamics of that relationship than the dynamics of intrinsic portfolio company growth.

{kind=link}